The Great Wealth Transfer: 6 Steps to Strengthen Your Business Before You Sell

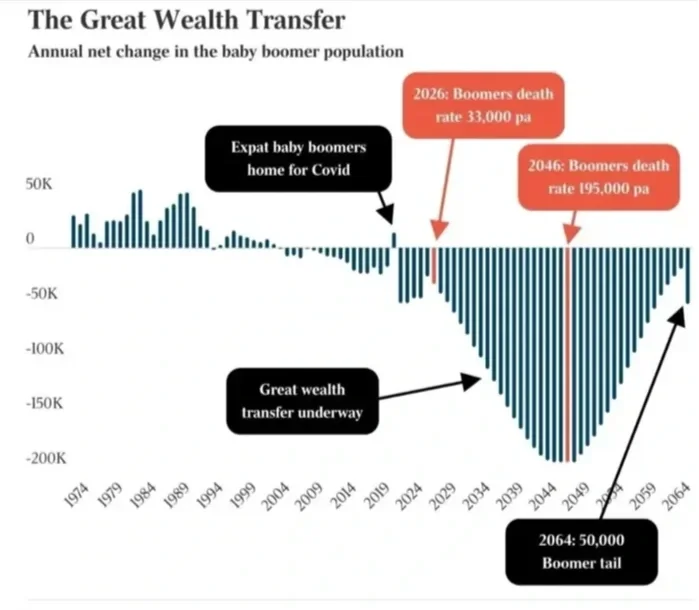

The Great Wealth Transfer; annual net change in baby boomer population NZ.

Over the next two decades, something significant is going to reshape the New Zealand business landscape. Baby boomers, who own a substantial portion of this country's small and medium businesses, are moving into retirement. The numbers are stark: by 2046, the boomer death rate is projected to reach 195,000 per year. The wealth tied up in those businesses has to go somewhere. Over this period New Zealand’s Baby Boomers are projected to pass on $1.6 trillion in wealth to the next generation.

This is what economists are calling the Great Wealth Transfer. And for business owners who are even beginning to think about an exit, whether that's in two years or ten, it raises an important question.

Is your business actually ready to sell?

Most aren't. Not because they aren't good businesses, but because being a good business and being a sellable business are two very different things. Here are six steps to start closing that gap.

1. Understand What a Buyer Is Actually Buying

This is the most important mindset shift an owner can make, and most never make it.

When a buyer looks at your business, they are not paying for what it has done. They are paying for what it will do — for them, without you. They are buying future earnings, future cashflow, and the confidence that those earnings are real, repeatable, and not dependent on the current owner walking through the door every morning.

If you start with this understanding, everything else on this list makes sense.

2. Get Your Financials Clean, Consistent and Bankable

Three years of clear, well-presented financial statements is the baseline expectation from any serious buyer or their advisors. But clean doesn't just mean accurate, it means normalised, transparent, and bankable.

Most owner-operated businesses run personal expenses through the company, pay the owner a salary that doesn't reflect market rate, or have one-off costs that distort the true picture. A buyer's accountant will adjust for all of this, but if you do it first, and present a normalised view of earnings, you control the narrative.

Think like a bank, not just a buyer

Here's a perspective most sale advisors miss: your financials shouldn't just satisfy a buyer, they should satisfy the buyer's bank. In most SME transactions, the buyer needs to borrow to complete the purchase. That means a credit analyst at a lending institution will assess your business through the same lens they would any lending application.

Your financials need to demonstrate:

- Debt Service Cover Ratio (DSCR) sufficient to service acquisition debt on top of existing obligations

- Interest cover and principal and interest cover that give a lender confidence in repayment capacity

- EBITDA that is clean, consistent and defensible under scrutiny

- Equity percentage that reflects a well-capitalised, well-managed business

- Margin trends that are stable or improving — not deteriorating

If your financials can walk into a bank as a ready-made lending application, you have removed one of the biggest obstacles to a completed transaction. Buyers who can get funded quickly are buyers who can move decisively — and that is in your interest as a vendor.

The balance sheet matters more than most owners realise

The P&L gets most of the attention in a sale, but a buyer's bank will scrutinise the balance sheet just as closely. Key considerations include:

- Shareholder current accounts — if you have been extracting value through a current account rather than salary over the years, this liability needs to be understood and ideally resolved before sale. A buyer does not want to inherit a complex current account structure, and a bank will view it as a risk. Work with your accountant to understand the implications and plan accordingly.

- Asset quality — are fixed assets appropriately depreciated, or is there a hidden capital replacement cost a buyer will face shortly after settlement?

- Liquidity — can the business fund its own working capital needs, or does it regularly require cash injection? A buyer's bank will want to see that the business is self-sustaining.

- Equity position — a strong equity base signals that the business has been well managed over time and provides security comfort to a lender.

Getting your balance sheet into good shape before going to market is not just about aesthetics. It is about removing friction from the transaction and giving both the buyer and their bank the confidence to proceed.

3. Reduce Owner Dependency

This is where many good businesses fall short in a sale process.

If your business relies heavily on your relationships, your knowledge, or your daily involvement — a buyer will price that risk into their offer, or walk away entirely. The question they are asking is: what happens to this business the day after settlement?

Practical steps to reduce dependency include documenting key processes, empowering staff to make decisions, transitioning client relationships to team members, and demonstrating that revenue is tied to the business — not to you personally.

This doesn't happen overnight. It is one of the strongest arguments for starting sale preparation years before you intend to sell.

4. Strengthen the Metrics That Drive Valuation

Businesses are typically valued as a multiple of earnings, most commonly EBITDA. That multiple is influenced by a range of factors, and understanding them gives you something to actively work on.

Metrics that support a stronger multiple include:

- Recurring or contracted revenue — predictable income is valued more highly than transactional

- Customer concentration — if one client represents 40% of revenue, that is a risk a buyer will discount

- Staff retention — low turnover suggests a stable operation that will survive a change of ownership

- Debt levels — a clean balance sheet with manageable debt is significantly more attractive to buyers and their lenders

- Systems and processes — a business that runs on documented systems rather than tribal knowledge is easier to value and easier to finance

If you know which of these are weaknesses in your business today, you have time to address them.

5. Understanding Your Starting Point — What Is Your Business Worth on Paper?

Before you engage a business broker or listing agent, it is worth understanding what your business looks like on paper. A broker will bring market expertise — comparable sales, sector multiples, buyer appetite — but they can only work with the numbers you give them. If those numbers haven't been properly prepared, the valuation they arrive at may not reflect the true value of what you've built.

There are two primary lenses through which a business can be assessed at this stage.

Normalised Earnings

The most common basis for SME valuation is a multiple of maintainable earnings — typically EBITDA, adjusted to remove one-off costs, non-commercial owner salaries, and personal expenses that have run through the business. This normalised figure represents what the business genuinely earns under normal operating conditions, and it is the number a buyer and their bank will scrutinise most closely.

Getting this figure right matters enormously. An under-normalised earnings figure — one that hasn't properly added back legitimate adjustments — can mean a vendor accepts a price that significantly undervalues their business. Conversely, an inflated figure that doesn't hold up to due diligence will erode buyer confidence and can derail a transaction entirely. The goal is an accurate, defensible number that you can stand behind.

Balance Sheet Value

Where a business holds significant tangible assets — property, plant, equipment, or a strong net asset position — the balance sheet provides an important floor for valuation. A business should rarely sell for less than its net asset value, and understanding that figure clearly gives a vendor a baseline below which they should not go.

This is also where the work done in Step 2 becomes critical. A clean, well-structured balance sheet — with shareholder current accounts resolved, assets appropriately valued, and liabilities clearly understood — presents a more compelling picture to both a buyer and their advisors than one that requires significant interpretation.

A Note on Market Valuation

It is important to be clear about the boundaries here. Determining what a business will actually achieve in the market — based on buyer demand, sector conditions and comparable transactions — is the domain of an experienced business broker or valuation specialist. That expertise is distinct and valuable, and engaging the right advisor at the right time is an important part of the sale process.

What accounting and financial analysis can do is ensure the foundation those market judgements are built on is as accurate and as strong as possible. A vendor who understands their normalised earnings, knows their balance sheet position, and has clean financials to present is a vendor who walks into a broker conversation — and ultimately a buyer negotiation — with clarity and confidence.

That clarity is often the difference between accepting the first offer and achieving the outcome you deserve

6. Structure the Deal to Get It Across the Line

Even a well-prepared business can face transaction friction if the deal structure isn't right. Two elements that are worth understanding early are vendor financing and handover arrangements.

Vendor Financing

Vendor financing — where the seller agrees to finance a portion of the purchase price on agreed terms — is more common in SME transactions than many owners realise, and it can be a powerful tool for both parties.

For a buyer, it bridges the gap when their bank won't lend the full amount. For a seller, it signals confidence in the business continuing to perform — and buyers and their banks view that positively. A vendor who is willing to leave money in the deal is a vendor who believes in what they're selling.

Typical structures involve the vendor holding 10–20% of the purchase price, repaid over an agreed period with interest. It is important to understand that a bank will usually require vendor financing to be subordinated to their own lending — meaning the bank gets repaid first. This needs careful legal and financial structuring, and should be discussed with your advisors early in the process.

Done well, vendor financing can accelerate a transaction, support a stronger headline price, and create alignment between buyer and seller through the transition period.

Handover and Continuity

The handover period is the human side of the transaction and it is where deals can quietly unravel after settlement if it hasn't been properly planned.

For most SMEs, a structured handover of three to six months is typical, though more complex businesses may require longer. The handover period should be clearly defined in the sale agreement, with milestones, expectations and the vendor's availability all documented.

Key elements of a successful handover include:

- Knowledge transfer — systems, processes, supplier relationships and operational know-how documented and communicated

- Client relationship transition — a clear plan for introducing the new owner to key clients, with the vendor actively facilitating rather than simply stepping aside

- Staff communication — handled carefully and at the right time, with the vendor endorsing the new owner's leadership

- Ongoing availability — many transactions include a consulting arrangement beyond the formal handover period, giving the buyer access to the vendor's knowledge on a part-time basis for an agreed fee

Where part of the purchase price is structured as an earnout — tied to post-settlement performance — the vendor has a financial incentive to ensure the handover is genuine and the business continues to perform. This can be a useful alignment tool, though it requires careful negotiation to ensure the metrics and timeframes are fair to both parties.

The businesses that achieve the smoothest transitions — and the strongest reputations in the market — are those where the vendor treats the handover as the final chapter of their leadership, not an afterthought to the transaction.

The Best Time to Start Is Before You Think You Need To

The businesses that achieve the strongest sale outcomes are almost never the ones that decided to sell and then started preparing. They are the ones that ran their business as if it were always ready to sell — clean financials, a bankable balance sheet, reduced owner dependency, strong metrics, and a clear picture of future potential.

The Great Wealth Transfer is already underway. The question isn't whether there will be buyers — there will be. The question is whether your business will be one that commands a premium, or one that gets discounted.

If you're beginning to think about your exit — even loosely — it's worth having a conversation about where your business stands today and what a preparation plan might look like.

ID Consultancy works with business owners to build financial clarity at every stage — from startup funding to exit readiness. Get in touch to start the conversation.